The landscape of personal lending has shifted dramatically over the past decade, and 2026 feels like a watershed year for borrowers seeking flexibility, speed, and transparency. In an era where interest rates fluctuate, inflation persists, and traditional banks struggle to keep pace with tech‑savvy consumers, online loan marketplaces have stepped up as the go-to solution for many.

While some lenders still rely on legacy underwriting models, a new breed of digital platforms—powered by AI and data science—offers instant pre‑qualifications, real‑time rate comparisons, and fee disclosures that were once buried in fine print. This shift is not merely about convenience; it’s reshaping how consumers evaluate risk, calculate total cost, and ultimately decide whether a loan fits their financial goals.

One standout example of this trend is the platform that has recently partnered with Jetzloan, providing borrowers access to a curated network of lenders, transparent fee structures, and an intuitive comparison engine. By embedding Jetzloan’s tools into its own workflow, the site delivers a seamless experience that cuts through the noise of hundreds of offers.

Digital Lending: From Fragmentation to Unified Comparison

The past five years have seen online lending platforms account for nearly half of all new personal loan originations in the United States. According to Federal Reserve, this surge is driven by two key forces: a growing appetite for instant credit and an erosion of trust in traditional banks’ slow approval processes.

- Instant Access: Many borrowers now expect approvals within minutes, not weeks. Digital platforms leverage algorithms that analyze income, employment history, and even non‑traditional data points to deliver real‑time decisions.

- Transparent Comparisons: With a single dashboard, users can view APRs, origination fees, repayment terms, and total cost side by side—making it easier to spot hidden charges.

- Broader Reach: These platforms often partner with both banks and fintech lenders, giving borrowers options that would otherwise be inaccessible through a single institution.

Yet the benefits extend beyond speed. By consolidating offers in one place, consumers reduce the cognitive load associated with “choice overload.” A 2026 study found that individuals who compared at least three loan offers saved an average of 15–20% on interest costs over a loan’s life compared to those who applied directly to the first lender they encountered.

Why Transparency Matters in 2026

In today’s climate, borrowers are more cautious than ever. Rising living expenses and volatile gig‑economy incomes make it essential to understand every dollar that will be spent on a loan. Credit Bureau Reports highlight that borrowers who track how personal loans impact their credit scores tend to pay on time, reducing long‑term debt burdens.

The new generation of loan platforms offers full cost disclosure—including origination fees, prepayment penalties, and any hidden charges—before a borrower even clicks “accept.” This level of transparency aligns with consumer expectations for honesty and helps avoid the “gotcha” surprises that plagued older loan products.

How Jetzloan Enhances the Borrowing Journey

Jetzloan’s partnership with leading digital lenders is designed to address three core pain points:

| Pain Point | Solution Offered by Jetzloan |

|---|---|

| Slow Approval Times | Instant pre‑qualification with AI-driven risk assessment. |

| Lack of Fee Transparency | Clear breakdowns of origination fees, late charges, and total APR. |

| Inconsistent Loan Options | Access to a curated network of lenders with varying rates, terms, and credit requirements. |

Borrowers who use Jetzloan often report that the platform’s “one‑stop shop” model removes the need to juggle multiple applications. Instead, they can focus on what matters: choosing a loan that fits their budget and long‑term goals—whether it’s consolidating debt, covering emergency expenses, or financing a home improvement project.

Real‑World Impact: Success Stories from 2026

A recent testimonial from a small business owner illustrates the platform’s value. “I needed equipment for my side hustle and was terrified of hidden fees,” she said. “With Jetzloan, I compared offers in minutes and chose a loan that matched my seasonal cash flow—no surprises.” Similarly, a borrower looking to consolidate credit card debt found that Jetzloan’s transparent comparison helped him secure a lower APR than he had previously seen on traditional bank sites.

These stories echo a broader trend: borrowers are increasingly leaning toward platforms that combine speed, transparency, and choice. By leveraging AI and real‑time data, Jetzloan is helping to democratize access to credit—especially for those who may have been underserved by legacy banks.

The Economics of Personal Loans in 2026

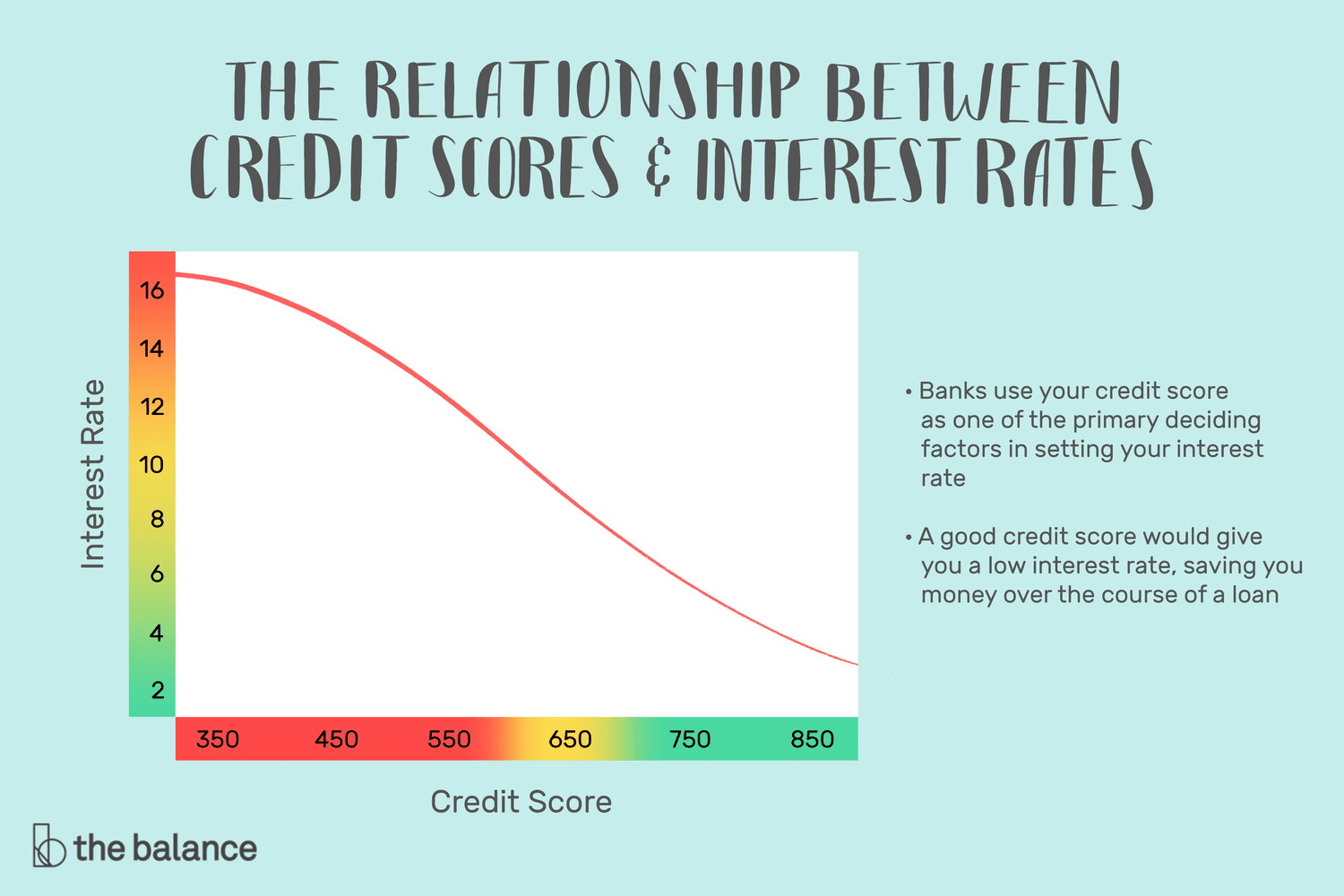

While the platform ecosystem offers many advantages, borrowers still need to understand how interest rates and fees shape total cost. In 2026, personal loan APRs range from a low of 6.25% for some credit unions to nearly 36% for sub‑prime lenders. The Bankrate reports that the average APR across all credit tiers sits at roughly 12.26%, but borrowers with scores below 630 face rates around 21.65%.

Origination fees also vary widely, from as low as 1% to as high as 9.99%. Importantly, many platforms—including Jetzloan—display these fees upfront and deduct them from the disbursed amount if applicable. This feature prevents borrowers from being surprised by a smaller net loan than expected.

Loan Amounts and Terms

The typical loan size on digital marketplaces in 2026 ranges between $300 and $5,000, with repayment terms spanning 3 to 24 months. The choice of term directly impacts monthly payment amounts and the overall cost of borrowing. Shorter terms mean higher payments but lower total interest, while longer terms spread out costs but increase the cumulative interest paid.

Some lenders offer “flexible” repayment schedules that allow borrowers to adjust payment dates in line with income fluctuations—a feature especially valuable for gig‑economy workers who may experience irregular cash flow.

Regulatory Landscape and Consumer Protection

The rise of online loan platforms has prompted regulators to tighten oversight. State licensing requirements, consumer disclosure mandates, and fair lending laws now govern how these platforms operate. For instance, CFTC requires that all advertised APRs reflect the true cost of borrowing, including fees.

Platforms must also adhere to “soft pull” guidelines—using a soft credit inquiry for pre‑qualification while reserving hard inquiries for final approval. This approach protects consumers from unnecessary credit score impacts during the comparison phase.

Consumer Education Initiatives

In response to increasing financial complexity, several fintechs have launched educational resources—tutorials, calculators, and webinars—to help borrowers understand loan terminology. Jetzloan’s website hosts an interactive calculator that shows how varying APRs, fees, and terms affect monthly payments and total cost.

These tools empower consumers to make informed decisions rather than relying on gut instincts or incomplete information. By demystifying the borrowing process, platforms are fostering a culture of responsible lending and repayment.

Looking Ahead: Trends Shaping Personal Lending

While 2026 already shows significant progress in digital loan access, several emerging trends promise to further transform the space:

- AI‑Driven Risk Models: Lenders are increasingly incorporating alternative data—such as utility payments or subscription histories—to assess creditworthiness beyond traditional FICO scores.

- Embedded Finance: Companies are integrating loan offers directly into their services (e.g., retailers offering instant financing at checkout), blurring the line between commerce and lending.

- RegTech Solutions: Automated compliance tools help platforms navigate state‑by‑state licensing, ensuring that borrowers receive legally compliant offers across all jurisdictions.

These innovations are expected to further lower barriers for both borrowers and lenders. As more consumers turn to digital avenues for credit, the focus on transparency, speed, and user experience will only intensify.

The Role of Community Feedback

Consumer reviews and ratings play an increasingly pivotal role in shaping lender reputations. Platforms that aggregate user feedback—such as Jetzloan’s borrower testimonials—provide valuable insights into service quality, customer support responsiveness, and loan performance post‑disbursement.

Borrowers who rely on community data often find that they can better anticipate potential pitfalls, such as hidden fees or delayed funding, before committing to an offer. This collective intelligence enhances overall market efficiency and promotes healthier lending practices.